Citycon: The Future (Of Retail Real Estate) Is Now, Old Man (OTCMKTS:COYJF)

sonatali/iStock Editorial via Getty Images

Despite its operational resilience and the quality of its portfolio, Citycon Oyj (OTCPK:COYJF) is still trading at a 23% discount from its price in early 2020. Citycon’s management is determined to close the 40% gap between its stock price and the company’s net asset value, by repurchasing shares and realizing the existing building rights. Hence, investors have the opportunity to acquire a quality real estate portfolio with a sweet upside potential.

Background information

Citycon Oyj (Citycon thereafter) is a real estate company founded in 1988 and operating in the Nordic and Baltic regions. The company is headquartered in Espoo (Finland) and has 233 employees. Citycon’s business model is centered on the active management and development of a portfolio of grocery-anchored community centers in major urban hubs. The company is not operating under a REIT-like regime, which allows for more flexibility in operations and earning reinvestment choices.

Citycon’s portfolio is composed of 39 properties valued at €4.46 bln. (third-party valuation by CBRE and JLL), including 37 shopping centers (€4.16 bln.) and one retail JV investment (€0.25 bln.). This represents a gross leasable area of 1,190 thousand square meters (sqm), with a solid occupancy rate of 94% and a weighted-average lease term (WALT) of 3.2 years, as of Q3 2021. The properties are located in Finland & Estonia (~43% of portfolio value), Norway (~34%) and Sweden (~23%).

Overview of financials

Citycon’s portfolio is generating a gross rental income (GRI) of €304 mln., a net operating income (NOI) of €209 mln. and funds from operations (FFO) of €104 mln., over the last 12 months (LTM) until Q3 2021 (including the proportionate share of its JV). The dividend policy consists in distributing 50% of the company’s normalized net income (i.e., net income after removing the changes in properties’ fair value). This results in a 7.0% dividend yield on the current stock price.

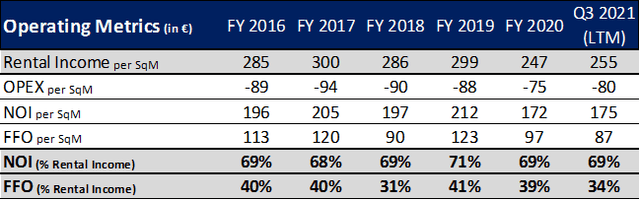

From FY 2016 to FY 2019, Citycon’s rental income was very stable around €290 per sqm, despite the difficulties experienced by the retail real estate sector in most developed countries. During the first year of the pandemic (FY 2020), the rental income fell at €247 per sqm (-17.4% year-over-year). However, over the LTM ending Q3 2021, the company presented a rental income of €255 per sqm, which seems to indicate that the situation has stabilized.

Interestingly, the NOI stayed remarkedly stable in percentage of the rental income (69.5% during FY 2020 and 68.8% for LTM Q3 2021, against an average of 69.1% from FY 2016 to FY 2019), attesting to the company’s ability to reduce its operational expenses. Citycon’s funds from operations (FFO) was also quite robust during the pandemic, most notably as a percentage of the rental income.

Created by author using company financials

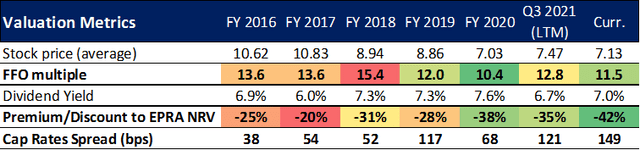

Citycon’s stock trades at €7.13 per share, at market close on January 10, 2022. This price is 23% under the prices in early 2020 (i.e., before the Covid-19 crisis), which averaged roughly €9.30. The stock traded as low as €5.30 during the crisis (43% drawdown), which implies a recovery of 35% since then. This can be put in perspective with Citycon’s EPRA NRV which falls by 5.7% from €12.3 per share (Q4 2019) to €11.6 per share (Q3 2021).

With a market capitalization of about €1.2 bln., the current stock price implies an FFO multiple of roughly 11.5x and an implied capitalization rate of 6.9%. This market-implied capitalization rate compares very favorably with the capitalization rate determined by the third-party valuers (at 5.4% based on company’s disclosure), resulting in a 149 basis points (bps) spread. Note that the public-private capitalization rates spread has materially widen, from FY 2016 to Q3 2021 (from 38 bps to 149 bps). This means that listed market investors are far more pessimistic than appraisers regarding Citycon’s properties’ fair value.

Created by author using company financials

Note 1: The numbers in the column “Curr.” are computed using the current stock price of €7.13 (10-Jan-2022) and company financials over the LTM ending Q3 2021. The other columns use the average stock price over the period and the company financials over the corresponding period.

Note 2: Cap Rates Spread (bps) is the difference between the capitalization rate which is implied in the stock price and the weighted-average capitalization rate used by the third-party appraisers to value the company’s properties (as disclosed in their financial reports). As such, this is a measure of the discrepancy between the private and the public markets’ perceptions of the fair value of Citycon’s assets.

Investment Thesis

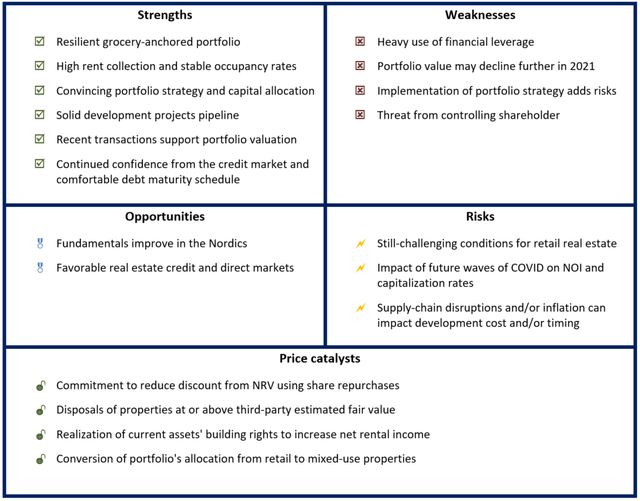

The following table summarizes the key points should be considered when analyzing Citycon.

Author

Strengths

Resilient grocery-anchored portfolio

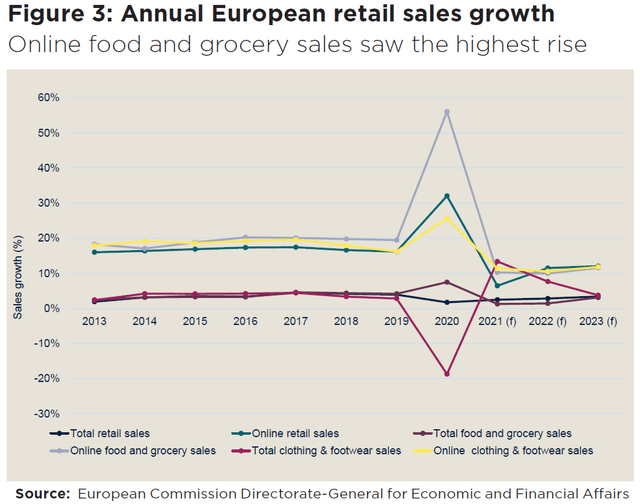

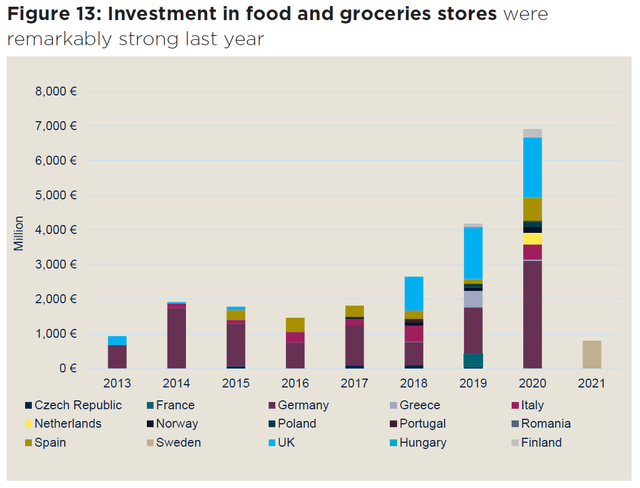

Groceries and other necessity-based retail (e.g., health care, dentists, pharmacies, etc…) are well known to be more resilient to change in consumers’ demand, notably during periods of economic stress. The Covid-19 crisis provided a perfect example of the resilience of grocery sales. As can be seen on the figure below, food and grocery sales were not much impacted in Europe, during the Covid-19 crisis.

Savills Research

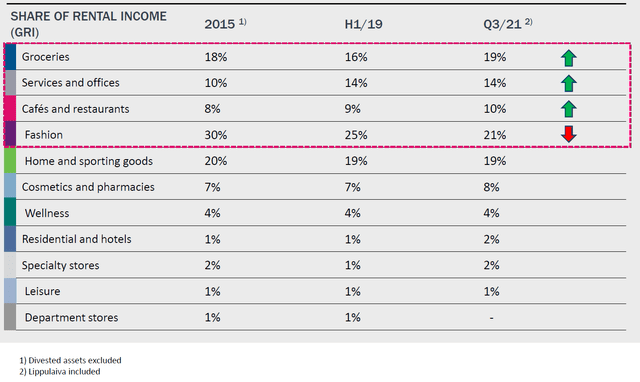

As of Q3 2021, grocery and necessity shopping represented roughly 37% of the total gross rental income of Citycon. This helped to maintain footfall (i.e., consumers’ traffic) and tenants’ sales in the company’s shopping centers. Moreover, footfall has a positive spillover effect on the other tenants which provide non-necessity goods or services (e.g., fashion retailers), as it drives potential consumers in centers. Service and office surfaces are also stable sources of rental income (14% of GRI).

Citycon

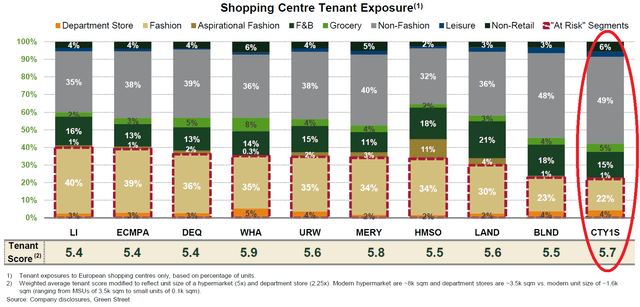

This orientation toward necessity-based retail combined with the fact that Citycon’s properties are well connected to public transportation networks contribute to stabilizing the company’s rental income. Importantly, this strategic orientation results from a still-ongoing effort by the management to minimize operational risk. As a result of this strategy, Citycon presents less rental income risk than its peers, as can be seen on the figure below. GreenStreet Advisors have found that Citycon has the lower exposures to “at-risk” segments among its European peers (based on rental units instead of GRI).

GreenStreet Advisors

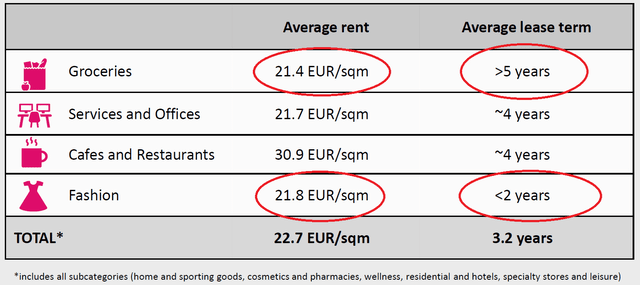

Grocery and other necessity-based tenants provide also advantages in terms of leasing. In comparison with fashion, grocery and necessity-based leases are generally longer and with a higher probability of prolongation, despite the fact that rents per sqm are at comparable levels. For groceries in particular, tenant’s credit risk is generally lower than for fashion, due to more stable revenues. Grocery shops also use bigger and less desirable areas, which help keep vacancy low. All these elements contribute greatly to stabilize the NOI of grocery-anchored properties. Note also that 92% of Citicon’s rental income is indexed to CPI, which provides protection against inflation.

Citycon

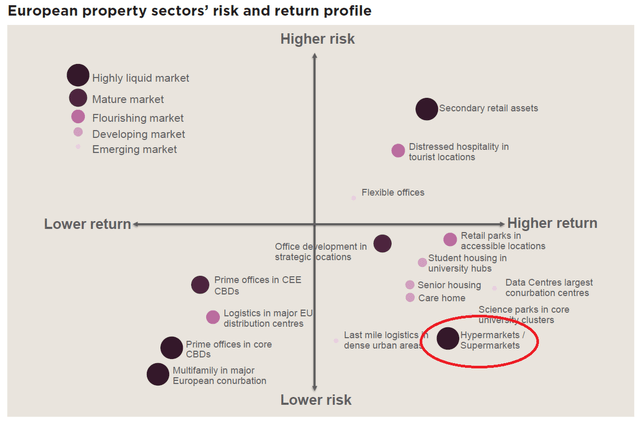

These advantages in comparison with fashion-oriented retail properties push investors to increasingly consider the food and grocery sector as the new core segment for retail real estate. According to Savills Research, this results in high return potential and limited risk, for this sector.

Savills Research

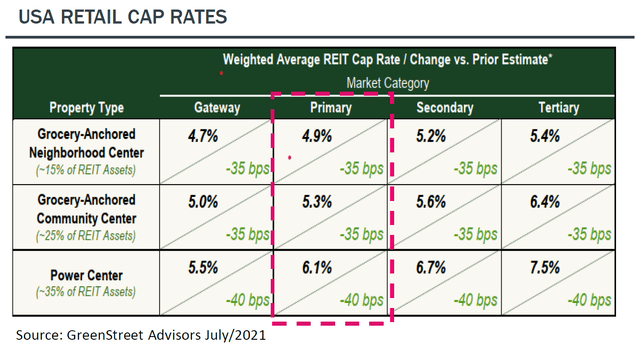

This perceived lower risk is generally translated in property valuations. On the U.S. market, Real Estate Investment Trusts (REITs) with grocery-anchored assets command a valuation premium of roughly 80 bps over other retail REITs (i.e., Citycon’s assets can be classified as grocery-anchored community centers).

Citycon’s “Capital Markets Day 2021” presentation

This premium is also generally present on the European direct market, where grocery-anchored properties present cap rates in line with the ones of prime centers (~100 bps under second class centers). On the European listed real estate market, the lower cash-flow risk of grocery-anchored assets is not priced. This puts Citycon at a relative pricing advantage in comparison with some of its peers.

High rent collection and stable occupancy rates

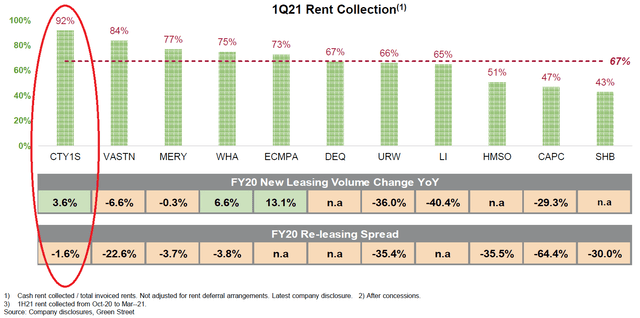

Citycon’s focus on stable retail properties has permitted to stabilize its rent collection and occupancy rates over time and, notably, through the pandemic. As such, its rent collection compares very favorably with its peers (consistently over 90% since FY 2016). As can be observed in the figure below, Citycon’s new leasing volume and re-leasing spread are comparatively stronger than its peers, during FY 2020. These numbers mean that Citycon was able to carry on with their leasing activity without conceding substantial discount on leases. This testifies to the strong demand for Citycon’s surfaces.

GreenStreet Advisors

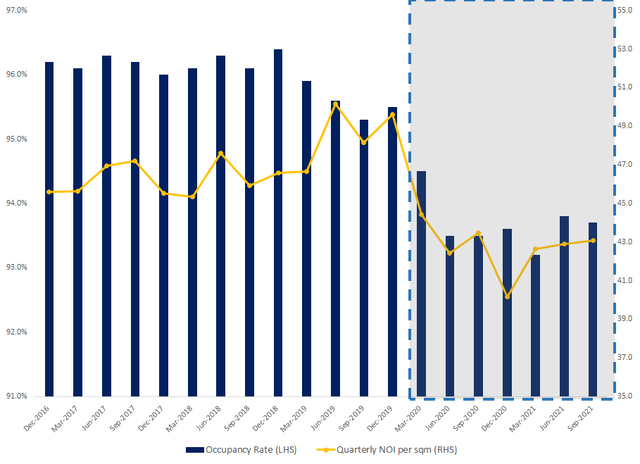

Before the Covid-19 crisis, occupancy rates were consistently in a very narrow range from 95% to 97%, since FY 2016. The pandemic had only a moderate impact on occupancy, which dropped to around to 93.5%. A level which is still very comfortable (peers’ occupancy rates were under 90%). This has reflected positively on Citycon’s quarterly NOI per sqm which fluctuates between €44 to €50 and €40 to €44, before and during the pandemic, respectively (excluding Kista Galleria JV).

Created by author using company financials

The business-friendly management of the pandemic in the Nordics (i.e., comprehensive support for tenants and less severe lock-downs than other European countries) helped to keep rental relief granted to tenants at a very low level of €5.2 mln., since the beginning of the pandemic (~1.8% of annual GRI). The total adverse impact of the Covid-19 on net rental income (i.e., rental relief, credit losses and loss of volume-driven income, such as parking) is estimated at €13.5 mln. and €5 mln. in 2020 and 2021, respectively.

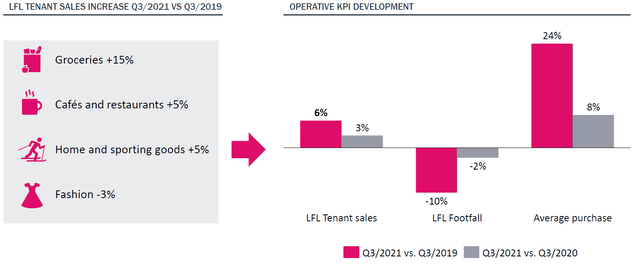

The softer approach taken by Nordic countries against Covid-19 also helped to minimize the impact on footfall. In 2020, Citycon’s centers welcomed 150 mln. visitors (down 16.8% from 2019, on a like-for-like basis). In Q3 2021, footfall was still down 10% against Q3 2019. Due mainly to groceries, the fewer number of visits was partially offset by a higher average spending per visit. This supported tenants’ sales, which were down only 3.7% year-over-year in 2020 (like-for-like basis). Sales were up 2.2% for the three first quarters of 2021, against the same period the year before (like-for-like basis).

Citycon

Convincing portfolio strategy and capital allocation

With 39 properties for a total estimated value of €4.46 bln. (as of Q3 2021), Citycon’s portfolio provides an adequate trade-off between being concentrated in a single strategy and having sufficient breadth to diversify away most of the properties’ idiosyncratic risk. Being positioned as a pure play investment in grocery-anchored community centers allows Citycon’s management to focus only on their core domain of expertise and this helped the company to weather the pandemic. The company’s assets are located in the Nordics’ largest urban areas, which are home to a growing share of the region’s population (currently, roughly one third of the Nordics population leaves in the largest urban areas and it is still increasing).

Citycon’s portfolio strategy can be described as a stable asset base with organic growth opportunities generated through the densification of the existing properties. Development generally targets mixed-use properties. This means adding residential, office and other surfaces (i.e., gyms, libraries, municipal services, etc…), which will drive traffic in the existing retail part of the property. This helps to make properties more resilient to economic shocks. A recent interview of F. Scott Ball (Citycon’s CEO), in EPRA Industry Magazine, provides a great overview of the company’s strategy and its approach to ESG-related matters.

Citycon

This portfolio strategy is well supported by the management’s disciplined allocation of capital. During the ” Capital Markets Day” presentation on November 16, the company’s management seems particularly concerned by the substantial discount of share price to EPRA NRV (~40%) and its implication on capital allocation. Non-core asset disposals at or above fair price is one proposition to raise funds that was brought forward by the management, as an alternative to more expensive equity offerings (see slide 74 in presentation). In itself, this is a very positive signal and this seems to indicate that the management is putting shareholders’ interest (i.e., closing the gap between share price and NRV) before their own interest (i.e., asset gathering)

In 2021, Citicon divested properties for a total of roughly €250 mln. The sale of 3 centers in Sweden (Stockholm area) for €147 mln. was realized in Q1 2021 and an additional center (Columbus center in Helsinki) was sold in Q4 2021 (sale agreement signed for €106.2 mln.). This is an attractive way to raise cash as the assets are sold at capitalization rates around 5.5%, when Citycon’s implied capitalization rate is currently over 6.9% (based on its stock price). Further asset disposals are planned in FYs 2022 and 2023 for €50-100 mln. per year. Part of the proceeds of these sales will be used to finance the development of existing properties. Capital expenditures for these developments are planned to be in the €160-180 mln. range in 2021 and around €100-150 mln. per year, in the foreseeable future (i.e., up to 2024).

Management also plans to use part of the asset disposals’ proceeds to repurchase shares at discount to NAV. During Q4 2021, Citycon has purchased 9,5 mln. shares (or 5.34% of the total number of shares) for €65.8 mln., that is an average share price of €6.93 (40% discount to EPRA NRV). All of these shares were subsequently cancelled by the company. Additionally, the repurchase of 0,5 mln. shares is currently ongoing. Obviously, these constitute very shareholder-friendly allocations of capital that should help to close the gap between share price and NRV.

Solid development projects pipeline

As mentioned above, Citycon generates value mainly by repositioning and developing further its already existing portfolio of core properties. This approach to value creation is intrinsically less risky than ground-up development, as the properties are already generating cash-flows and demand for the new surfaces can generally be better gauged. Hence, focusing on developing existing assets is a prudent approach to a risky venture (i.e., real estate development) and it is quite consistent with Citycon’s core portfolio strategy, where the company targets resilient grocery-anchored assets (i.e., a prudent approach) in the retail property market (i.e., a risky venture).

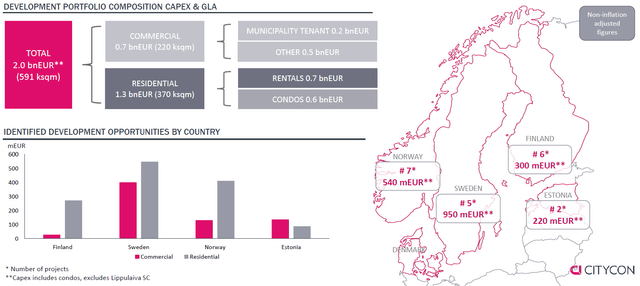

As of Q3 2021, Citycon’s pipeline comprises 20 potential development projects for total capital expenditures of roughly €2.0 bln. This represents roughly 590 thousand sqm in gross leasable area (GLA), which corresponds to 49.6% of existing GLA. Interestingly, more than half of the capital expenditures will be directed to residential assets. This pool of projects represents a potential value creation of €850 mln, or €2.3 per share (see valuation below for details on the valuation of this pipeline).

Citycon

Recent transactions support portfolio valuation

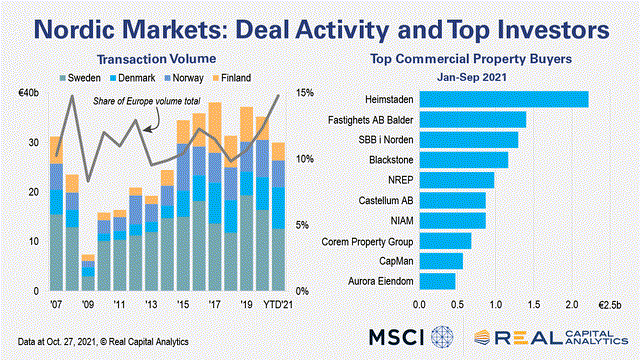

The appeal of the Nordics for real estate investors can notably be attributed to the resilient macroeconomic fundamentals of these countries, which are reflected by their solid sovereign credit ratings (Norway, Denmark and Sweden are all rated AAA by S&P, Finland is rated AA+ and Estonia AA- with positive outlook). These countries benefit from high GDP per capita, good growth prospect, low debt-to-GDP and high stability. According to CBRE, commercial real estate transactions in the Nordics are set for another record year in 2021 with a volume of €36 bln., as of Q3 2021 (against €44 bln. in FY 2020).

In contrast with the other leading real estate markets in Europe (i.e., UK, Germany and France), transaction volumes in the Nordics have been extremely stable during the pandemic and are currently over their 5-year averages (except for Finland). As of Q3 2021, the Nordics account for approximately 15% of the European commercial real estate transaction volumes. The resiliency of these markets have strengthened the place of the Nordics as a first-class investment destination for real estate investors.

Real Capital Analytics

As can be seen in the figure below, grocery-anchored properties have also experienced growing transaction volumes in Europe, over the past years. This can mainly be attributed to the perceived lower risk of these properties, in comparison with other retail sub-sectors.

Savills Research

This strong activity, both in the Nordic markets and for grocery-anchored properties, is highly positive for Citycon as it provides liquidity to divest non-core assets and it helps to support market prices. This has notably permitted Citycon to sell 4 assets during FY 2021 at prices at or above fair values. The first transaction (in Q1 2021) was the disposal of 3 properties for a price of €147 mln., which slightly exceeded the fair value of these assets as of Q4 2020. Then, the divestment of the Columbus center (repositioned as a necessity-based center) for €106.2 mln. in Q4 2021 represents a €10 mln. (or 10%) premium over its estimated value as of Q4 2020.

Weaknesses

Heavy use of financial leverage

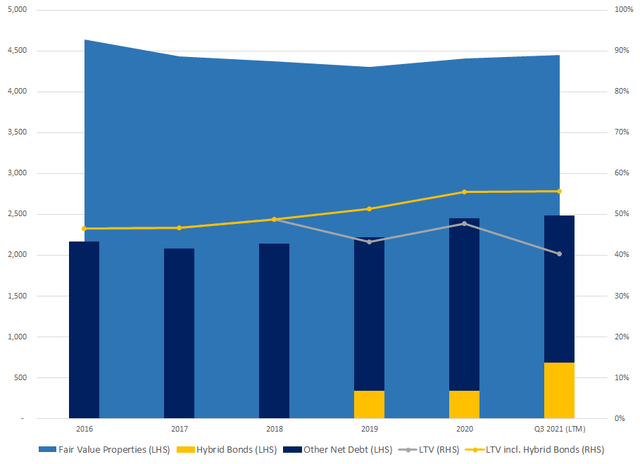

In contrast with its comfortable debt maturity schedule, the financial leverage used by Citycon flirts with the limit of what I consider as acceptable in regard to the portfolio’s risk. The company follows a stated maximum loan-to-value (LTV) target of 40-45%. As of Q3 2021, Citycon’s LTV (measured as net debt divided by the fair value of properties) was at 40%, down from 48% as of Q4 2020. Obviously, the increase in the fair value of the properties and the decrease in indebtedness (+1% and -0.8% since Q4 2020, respectively) are not sufficient to explain this drastic reduction in LTV.

In fact, this was mainly achieved by issuing a €350 mln. hybrid bond. Indeed, as permitted under IFRS rules, these hybrid instruments are classified as equity on the company’s balance sheet and, as such, are not taken into account in the LTV ratio.

The figure below displays some key metrics for Citycon, since FY 2016. As can be seen, the LTV computed as net debt divided by the fair value of properties is down at 40%, for Q3 2021. Over time, this ratio seems to indicate that the company is quite successful at reducing its leverage. However, if we correct this ratio to include the hybrid bonds issues (so, LTV = (Net Debt + Hybrid Bonds) / Fair Value of Properties), we get a quite different picture. Instead of going down, the LTV ratio slowly grows from 47% to 56%. To say the least, the management’s narrative that the company is successful at keeping its leverage under control is somewhat of an overstatement.

Created by author using company financials

Citycon’s heavy use of leverage requires to consider separately two components of financial risk, namely: rollover risk (i.e., the risk that the company will not be able to rollover or reimburse the principal of the bond at maturity) and coupon payment risk (i.e., the risk that the company will not be able to pay a coupon when due).

When assessing rollover risk, the LTV which excludes hybrid instruments (so LTV=40%) seems to be reasonable metrics, as these hybrid bonds are reimbursed at Citycon’s discretion. As such, these instruments do not materially impact rollover risk. Generally speaking, for stable companies in mature markets (as in the case of Citycon), difficulty to rollover debt can be due to deteriorating company’s fundamentals (notably properties’ quality for REITs/REOCs) or credit market conditions.

Considering the stability of Citycon’s underlying portfolio (as can be seen in the figure above), I would argue that a material deterioration in fundamentals (i.e., sufficient to prevent the rollover of debt) is a low probability event. It is notably hard to imagine that an investment-grade company with physical assets will not be able to rollover its debt at all. This seems especially true for Citycon as the company is issuing mainly regular medium-term bonds, by opposition with shorter-term commercial papers (which constitute only 3% of total indebtedness, as of Q3 2021). Moreover, the company’s assets are almost fully unencumbered, which is positive for unsecured creditors.

On the other side, credit market conditions at the rollover date are an entirely different beast. They are impossible to forcast and, as such, the credit spread at the rollover date is a big unknown. An important mitigating factor is obviously the well spread maturity schedule of Citycon, which limits the effect that a higher credit spread could have on the company’s aggregated financing cost. Considering the points above, I believe that the LTV of 40% is still at an acceptable level, despite being close to the limit at which I would not be comfortable anymore (45-50%).

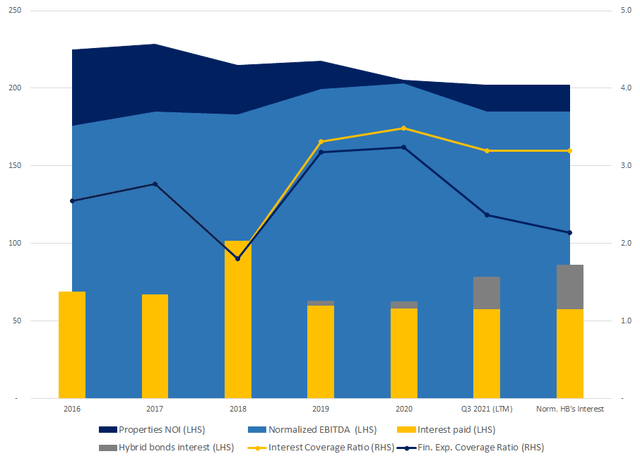

To assess coupon payment risk, it is now useful to account for hybrid bonds in indebtedness (LTV=56%). This LTV seems quite high, but it is not informative on a standalone basis. To get a full picture of coupon risk, I also computed interest coverage metrics, as can be seen on the figure below. The interest coverage ratios are computed as the regular bonds’ interests divided by the normalized EBITDA. The financial expenses coverage ratios are similarly computed, but it also includes hybrid bonds’ interests in the numerator.

Created by author using company financials

Note 1: The “normalized EBITDA” refers to Citycon’s Earnings Before Interest, Taxes, Depreciation, and Amortization (EBITDA), to which I added the net fair value gains/losses on investment properties, as this is not a monetary item. Indeed, these changes in the portfolio’s fair value (as estimated by third-party appraisers) have no impact on the company’s capacity to pay its coupon.

Note 2: The last column on the horizontal axis (labelled “Norm. HB’s interest”) shows the number for the LTM but with hybrid bonds’ financial expenses corrected to represent one full year of interest (i.e., as the second hybrid bond is issued in Q2 2021, its interest over the LTM represents only 3 months of interest instead of 12).

Note 3: The Kista galleria’s JV is fully removed from all the numbers above.

As can be seen in the figure above, properties’ NOIs and normalized EBITDAs are quite robust over time. Interest paid on regular bonds is ranging between €60 mln. and €70 mln. (with a notable exception in FY 2018). The hybrid bonds’ interest represents a growing financial burden of €28 mln. for a normalized year (€20 mln. for LTM ending in Q3 2021). Since FY 2019, the interest coverage ratio is at a comfortable level of ~3.3x, which is consistent with Citycon’s investment-grade rating.

On the other side, the financial expenses coverage ratio is decreasing to a level of 2.1x, when considering the normalized interest on hybrid bonds. This represents a fairly low coverage ratio considering the investment-grade status of Citycon and the illiquidity of its assets. However, I am still considering that the coupon payment risk is at an acceptable level, as the company benefits from a provision to defer interest payments on its hybrid bonds, “at any time and at its sole discretion”. (This provision can be found at page 43 of the prospectus of the 2025 hybrid bond. The 2026 hybrid bond should benefit from the same provision as mentioned in Fitch’s rating report for this issue.)

A property-focused valuation approach

Estimating Citycon’s intrinsic value requires to appraise both the NAV of the existing portfolio and the present value of future development projects. Note that the construction projects generate value from three sources: the fair value of the income-producing properties (net of construction costs), the profit margin on condominiums’ sales and, perhaps more importantly, the improvement in the market pricing of the NAV due to the lower risk of the portfolio (i.e., diversified REITs/REOCs trade at a lower discount to NAV than their retail counterparts).

For estimating the NAV of the existing portfolio, we need to determine the market NOI of the portfolio (i.e., the NOI resulting from all areas being leased at their market rent) and the appropriate capitalization rate. Note that the market NOI is intended to reflect the medium-term potential of the portfolio, this means that it does not incorporate the impact of short-term fluctuations. To take into account uncertainty in our valution, we use several assumptions pertaining to the value taken by these two inputs.

I derive market NOIs per sqm by using the ones implied in appraisers’ valuations (i.e., as the company discloses both the weighted-average yields used by the appraisers and the fair value estimates of its properties, we can derive the implied market NOIs per sqm). These implied NOIs are €202, €216 and €210 per sqm for LTM ending Q3 2021, FY 2019 and the average of FY 2016 to 2019, respectively.

Over the same periods, the realized NOIs were €175, €212 and €202 per sqm, respectively (note that LTM NOI at €175 is impacted by rental relief, which seems unlikely to persist over the long term). Hence, as presented in the table below, I elaborate five scenarios, with the “recovery” scenario as our base case. Assuming that operating expenses represent 31% of the rental income (average from FY 2016 to Q3 2021), we can calculate the implied market rent per sqm for our scenarios. Note that these implied rents are below the rental income per sqm of the pre-leased surfaces in Lippulaiva, a 44 thousand sqm property that Citycon is currently developing in Helsinki.

Created by author

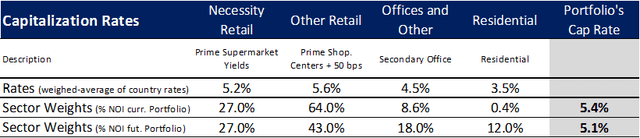

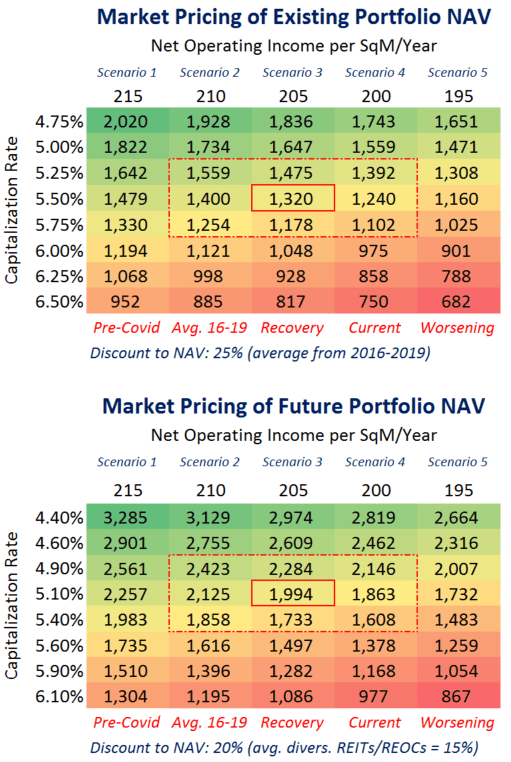

Our base case assumption regarding the capitalization rate is 5.5%, which is 10 bps over the weighted average required yield disclosed by Citycon’s third-party appraisers. Note that our base case capitalization rate was computed using published capitalization rates by country and Citycon’s portfolio sectoral/country allocation. As can be seen on the table below, Citycon’s aggregate capitalization rate will fall from 5.4% to 5.1%, when the new sectoral composition is considered (i.e., after development).

Created by author using data from Citycon, CBRE and Savills Research

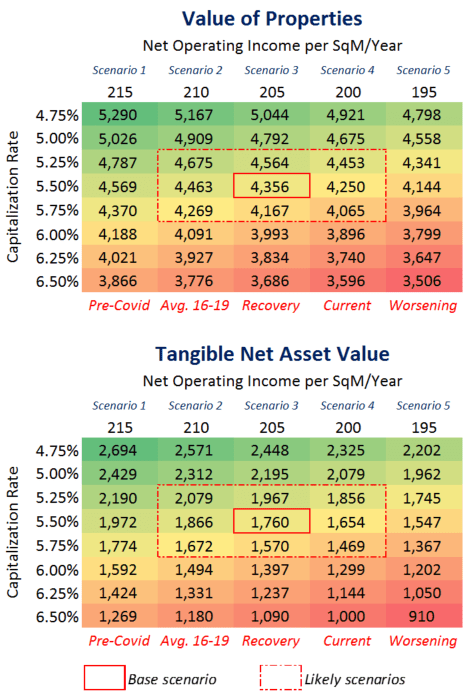

We can derive the NAV of Citycon’s existing portfolio under various inputs assumptions, as on the matrix below. The estimated properties’ value incorporates the 50% of Kista Galleria that is own by Citycon (i.e., JV consolidated using equity method on Citycon’s balance sheet), but it does not include the Columbus center, which was sold during Q4 2021. Note also that the computed NAV takes notably into account the debt from the Kista Galleria’s JV, the rest of the proceeds of Columbus disposal after the repurchase of shares, and the hybrid bonds.

Considering that Citycon has currently ~168.5 mln. shares outstanding, our base case scenario results in a NAV of roughly €10.4 per share for the existing portfolio (aggregate NAV of €1,760 mln.). Considering that the portfolio has historically traded at a 25% discount to its NAV (approximated using the EPRA NRV), this results in a target stock price around €7.8 per share (11% above the current stock price).

Created by author

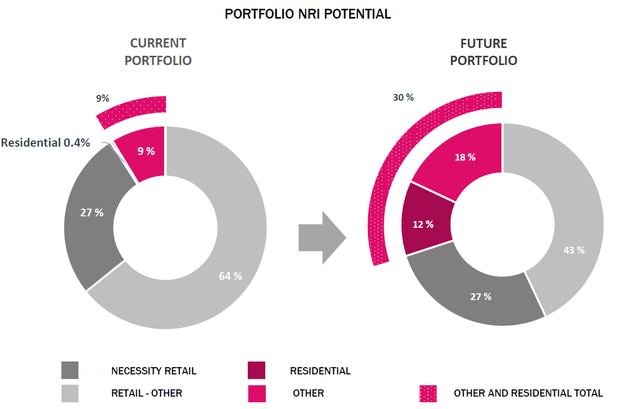

Yet, the above NAV computation does not take into account the potential upside that could be generated through the development of existing building rights. These represent roughly 419 thousand sqm of GLA (not including condominiums), which would increase Citycon’s aggregate GLA to 1,588 thousand sqm. More importantly, this would permit to substantially modify Citycon’s surface allocation.

The future net rental income will have the following sectoral composition: 27% for necessity-based retail, 43% for other retail, 18% of other surfaces (including office, library, municipal services, etc…) and 12% of rental apartments. These constructions will require capital expenditures of €1,400 mln., based on the company’s estimate. Additionally, Citycon has building rights that will be used to develop for-sale condominiums, for an estimated construction cost of €600 mln.

Citycon

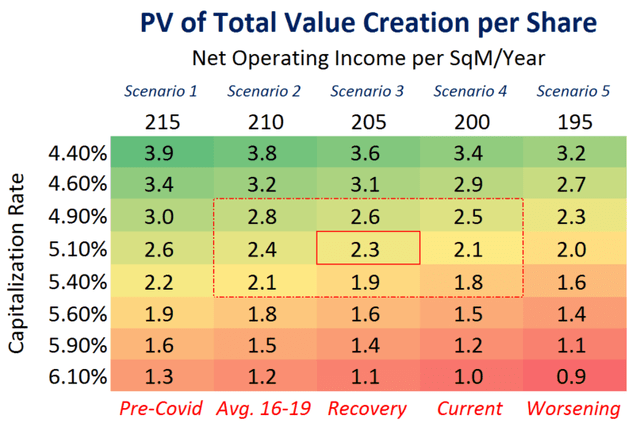

To value the development projects, we will assume that Citycon will develop fully its potential GLA (~419 thousand sqm) and that the new portfolio’s sectoral allocation will correspond to the expected allocation mentioned above. We will further assume that the NOI per sqm for each scenario will increase by 1% per annum due to inflation, over the construction horizon. We use the estimated capital expenditures of €1,400 mln., that we increase at a rate of 3.5% per annum (i.e., roughly 100 bps above the IMF’s expected inflation rate for the Nordics).

So, the aggregate construction cost for income-generating properties is €1639 mln. We will take for granted that the condominiums will generate a quite standard 20% profit margin over the estimated construction cost of €600 mln. (that I do not adjust for inflation). Finally, we will assume that both expenses and the value creation will be evenly spread over the construction time horizon (i.e. estimated at 8 years, instead of the 6 years expected by Citycon). The value created will be discounted at a rate of 20% per annum, which seems consistent with the risk inherent in this kind of venture.

These assumptions permit us to compute the NAV of the future portfolio and its market pricing. We will presume that the discount to NAV applied by market participants will decrease from 25% to 20%, due to the lower perceived risk of the portfolio (i.e., higher sectoral diversification and portfolio larger size). This discount is 50 bps lower than the current average discount to NAV observed on the market for diversified REITs/REOCs (i.e., a 15% discount to NAV).

Created by author

We can now derive the value generated through developments by substracting the market pricing of the existing portfolio NAV from the market pricing of the future portfolio NAV. As mentioned previously, we will then assume that this value is evenly generated over 8 years and discount it back to today (discount rate of 20% per annum). As such, we found that the present value (PV) of the total value creation is roughly €1.7, on a per share basis.

Created by author

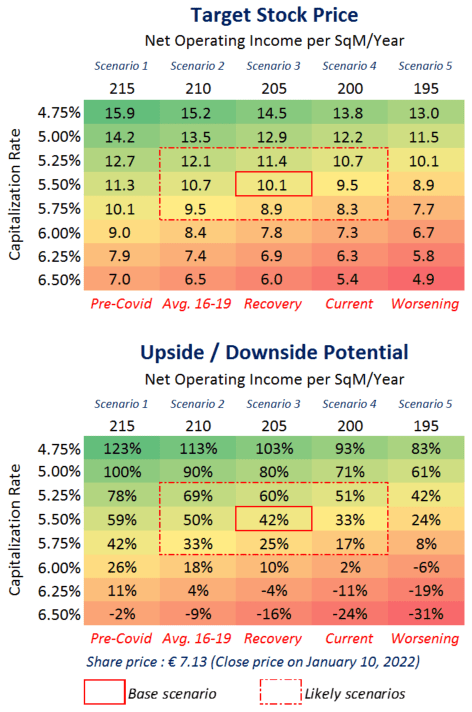

By adding the market pricing of the current portfolio NAV and the present value of the total value creation (both on a per share basis), we obtain our estimate of the intrinsic value of Citycon’s share (i.e., our target stock price). For our base case scenario, which assumed a recovery in NOI and a fairly stable capitalization rate, we obtain a target stock price of €10.1 (upside potential of ~42%). Our set of likely scenarios give us a range of target stock prices from €8.3 (+17%) to €12.1 (+69%).

Created by author

Conclusion

Citycon’s management seems to have both the capacity and the willingness to reduce the discount between the stock price and the company’s NAV. This objective could be achieved by the repurchase of shares using the proceeds of asset disposals and/or by the realization of existing construction rights.

Interestingly, Citycon’s management has decided to use both of these tools in conjunction. I am confident that Citycon has the necessary expertise to realize the buried value that the existing construction rights represent. Importantly, the value creation will not only come from the development of new surfaces, but also from the improvement in the pricing of the company due to the transitioning of the portfolio towards mixed-use.

At its current level of €7.13, Citycon’s stock seems inappropriately cheap. If the development potential of the company is carefully considered, Citycon’s stock should be priced closer to €10, which implies an upside potential of 40%. As such, I consider Citycon as a great opportunity to get exposure to a resilient portfolio of quality assets, with a comfortable upside potential.