French real estate firms’ pre-pandemic caution leaves breathing room for lenders

| French retailers in the Gobelins district of Paris have been hit hard by measures to prevent the spread of COVID-19. Source: Frédéric Soltan / Corbis News via Getty Images |

When France came to terms with another nationwide COVID-19 lockdown, tNon-food retail, hospitality and recreational property owners in particular face a long embargo when they could instead have been looking forward to the country’s tourism season opening during a busy Easter break.

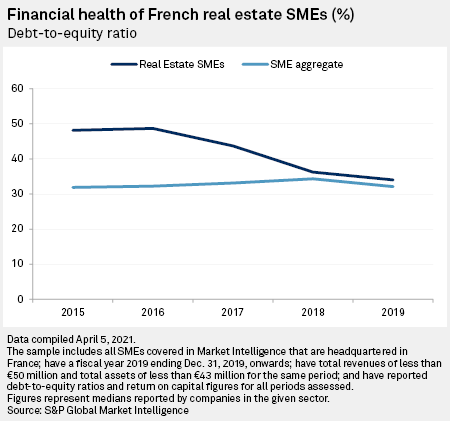

The blow will no doubt be hard to feel, but many real estate companies should take some comfort in the relative health with which they entered the pandemic. Data from S&P Global Market Intelligence shows that the median leverage of French small and medium-sized real estate companies fell from 48.16% in 2015 to 34.01% by the end of 2019.

“Most Investors generally to have been to attempt to manage Low you Debt versus equity relationship over recently Years, just to receive it in a position to protect yourself, “said Damian Harrington, director of research for Europe, the Middle East and Africa at real estate services company Colliers International, in an interview.”Of 2018 to 2019 all together was concerned The There was walk to Be something kind of [economic] wobble because we were all Long in the Cycle, but nobody Really knew What it was walk to Be.”

Real estate was the focus of the 2008 global “wobble” caused by loose loans to homeowners in the US. The contagion that later spread through the global financial system resulted in similarly ruthless lending to the commercial property sector in several key markets. Many real estate firms entering the crisis are heavily indebted.

For French real estate SMEs, at least, these lessons appear to have been drawn, as their average leverage ratio fell 14 percentage points in the five years to the end of 2019, according to Market Intelligence data. This is comparable to largely flat indebtedness for French SMEs in general over the same five-year period, albeit from a lower starting point.

After bottoming out in 2009, French real estate investments soared to € 20 to 30 billion per year between 2014 and 2018, before posting a record year in 2019, according to the real estate service provider, with € 37.6 billion invested in Ritter Frank. Due to the strength of the French market, Paris even overtook London as Europe’s most popular destination for office real estate investments.

“The thrust for French investment market it lead to French Investors generally dependent Fewer on Debt, “said David Bourla, chief economist and research director at Knight Frank.” You have a lot More reduced [loan-to-value] Conditions. “

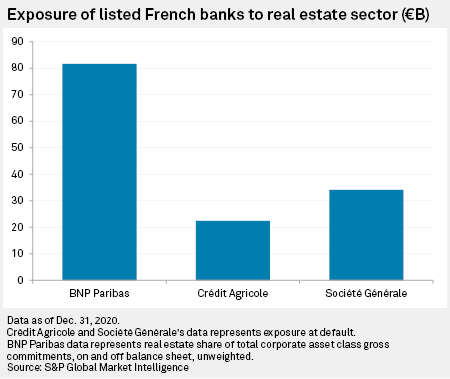

However, France’s main lenders remain heavily involved in this sector. BNP Paribas SA’s gross exposure to commercial real estate, which is mainly in Europe, was EUR 71.1 billion as of December 31, 2020, representing 3.9% of the Group’s total on-balance sheet and off-balance sheet commitments. Doubtful loans totaled EUR 1.64 billion, the company’s 2020 annual financial report found that represented 2.3% of the bank’s total exposure to the sector. The other two major French listed lenders, Crédit Agricole SA and Société Générale Société anonyme, had default risks of EUR 22.46 billion and EUR 34.13 billion, respectively.

While growing interest in French real estate in the years leading up to the pandemic helped bolster investor balance sheets, it also weighed on returns as competition for assets increased. The average return on investment of French real estate SMEs fell to 1.69% in 2019, from a high of 2.46% in 2015, according to Market Intelligence data. Overall, French SMEs saw a slightly smaller decrease in average returns on investment over the same period, but on a much larger basis.

“To the Years, aim returns [in real estate] to have been creeping in because the market has been just so much More competitive, “said Harrington. “”There are so much Capital out There.”

The damage COVID-19 has done to certain parts of the real estate sector has made the owners of that capital much more prudent.

“Buyer are increasingly carefully, how Well how Banker, when you are search at the a Asset to buy, “said Bourla.” you want to Be for sure The the Occupier is solid, and The There become Be a Well level of cash registerflow With The Asset. “

Non-food retail, hospitality and recreational properties have borne the brunt of the damage the pandemic has inflicted on the real estate market. Landlords are struggling to collect rent from tenants whose incomes have collapsed as customers stay away from their premises. UK-based retail landlord Hammerson PLC, which has a portfolio of retail properties in France valued at around £ 1.15 billion as of December 31, 2020, has only 58% of the first quarter rent of its French assets as of March 5 deducted.

“Sale is Where There are real question marks, “ said Harrington. “N.obody Really White Where This is Path, but values are certainly drop because results are To move out. N.obody Really White Where [retail] Rent are walk to to sit because everything is Be pushed toa revenue-based model. “

Owners of certain types of sub-prime real estate in regional cities – – the kind owned by real estate SMEs rather than large institutional investors – – Harrington added that they are also more vulnerable to the effects of the COVID-19 shock.

For French lenders, the real risk of their real estate exposure could be more indirect than it was during the global financial crisis, Harrington said. It is not so much the financial health of landlords that banks should be concerned about, but rather their tenants that they rely on to survive.

“There is possibly a liquidity blocking when it comes to Banks Lending to Company, “said Harrington. “D.ebt-to-Equity value Conditions to have Really Come in the [for real estate investors]so There is not Really a risk There. It is more over the Tenant pay rent – – to do you to have the Capital to keep going? “